VIX0.00+0%

SPX0.00+0%

NDX0.00+0%

VVIX0.00+0%

SKEW0.00+0%

SPY0.00+0%

QQQ0.00+0%

IWM0.00+0%

DIA0.00+0%

VIX0.00+0%

SPX0.00+0%

NDX0.00+0%

VVIX0.00+0%

SKEW0.00+0%

SPY0.00+0%

QQQ0.00+0%

IWM0.00+0%

DIA0.00+0%

VIX0.00+0%

SPX0.00+0%

NDX0.00+0%

VVIX0.00+0%

SKEW0.00+0%

SPY0.00+0%

QQQ0.00+0%

IWM0.00+0%

DIA0.00+0%

>SIMULATION: REAL-TIME

>MODEL: BLACK-SCHOLES

>VISUALIZATION: INTERACTIVE_3D

>ANALYSIS: GREEK_SENSITIVITY

STRATEGY DATABASE

Visualization

Module: Visualization

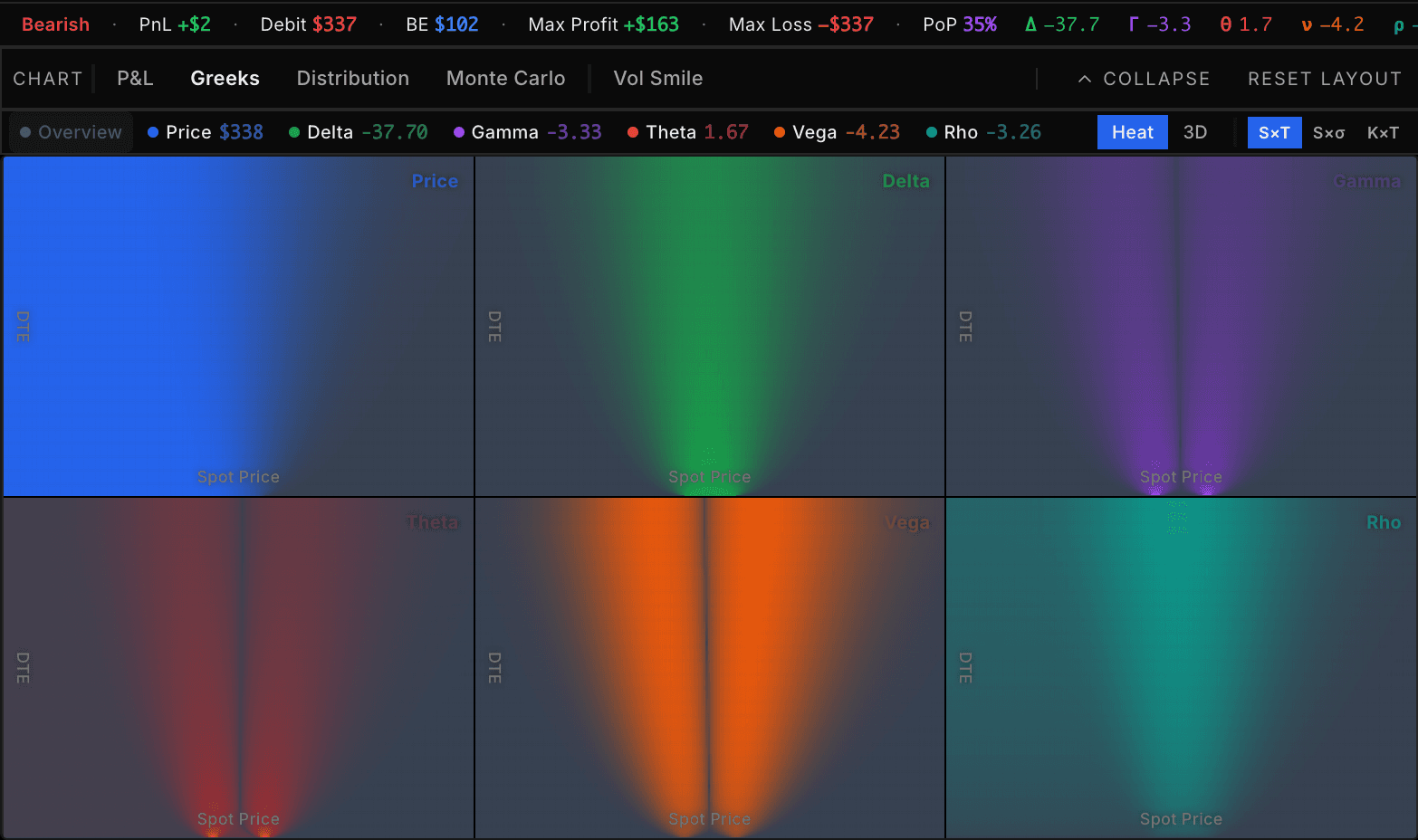

Visualize The Greeks

Don't just calculate Delta. Visualize the entire volatility surface. Our interactive 3D heatmaps allow you to see exactly how Theta decay and Gamma risk evolve over time and price.

POS: ATM STRADDLE

LONG_VOL // GAMMA_SCALPER

Spot Price

DTE

PRICE

Spot Price

DTE

DELTA

Spot Price

DTE

GAMMA

Spot Price

DTE

THETA

Spot Price

DTE

VEGA

Spot Price

DTE

RHO

Structures

Risk

Module: Risk

Probabilistic Risk

Move beyond linear Greeks. Run high-performance Monte Carlo simulations directly in your browser to model tail risks and visualize the full distribution of potential outcomes at expiration.

Monte Carlo Engine

Stochastic Path Simulator— Profit paths— Loss paths— P5 / P50 / P95

PATHS

2,000

SIM STEP

DAILY

CVaR (95%)

$84

Core Architecture

Interactive Stack

Built on a modern React framework for high-performance interaction. All Greek calculations and risk simulations are performed locally in your browser, ensuring instant feedback without server latency.

- Real-Time Sensitivity Analysis

- Client-Side Black-Scholes Engine

- Responsive Risk Visualizations

ENGINE: BLACK-SCHOLES V2

System Feedback Loop

Volatility Paradox is an evolving protocol. We rely on trader intelligence to refine our models and expand capabilities.

Latency

< 50ms

Pricing Engine

Black-Scholes

Risk Model

Monte Carlo

Strategy DB

20+ Templates

Data Coverage

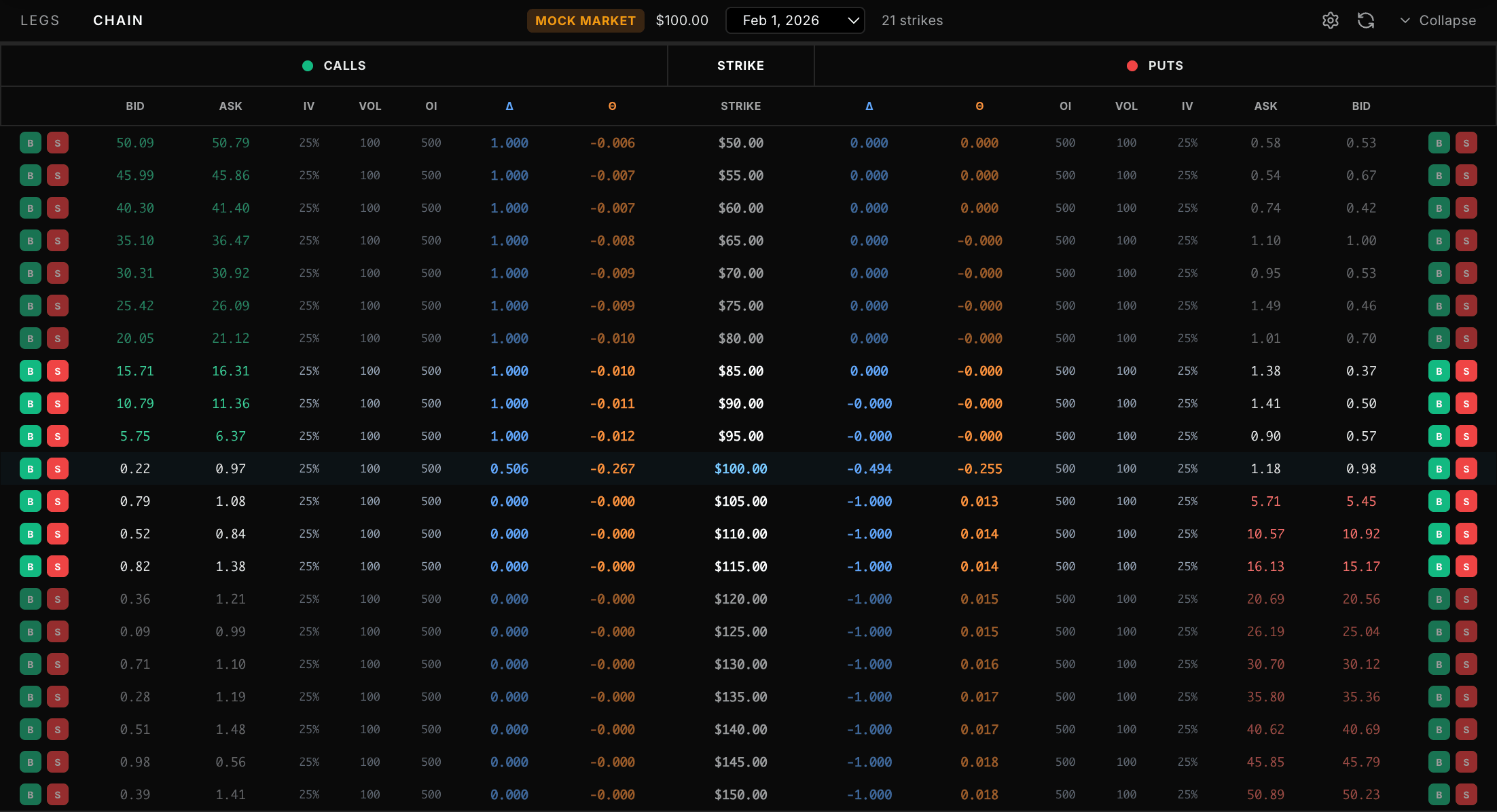

Real-Time Chain

Architecture

Next.js / Tensor

Terminal Access

Full access to the Black-Scholes pricing engine, 3D volatility surfaces, and risk modeling tools.

Strategy Library

Access 20+ pre-built institutional strategy templates. Iron Condors, Butterflies, and more.

Browse Templates